Understanding Fixed Indexed Annuities (FIAs)

Don’t Be Sold. Be Informed.

Safety-first growth with the option for lifetime income.

A Fixed Indexed Annuity (FIA) is an insurance contract designed to protect your principal while giving your savings room to grow. Your interest is linked to a market index (like the S&P 500®), but in any crediting period (usually one year, depending on the contract) you’ll never earn less than 0%. That blend of no-loss protection with measured upside makes FIAs a popular choice for people nearing or in retirement.

Get the latest FIA rate updates — no signup required

Need to review an existing annuity?

How FIAs Work (Simple Mechanics)

You deposit funds with a highly regulated insurance company.

Interest credits are tied to an index (like the S&P 500®) and subject to cap, participation rate, spread, and fees (varies by contract).

- Cap: A ceiling on the interest you can earn in a crediting period. If the index rises above the cap, you receive the cap; if it rises less, you receive the smaller amount (never below 0%).

- Participation Rate: The percentage of the index gain you’re credited. For example, at 50% participation and a 10% index gain, you’d earn 5% (before any spread/fees).

- Spread: A set percentage subtracted from the index gain before interest is credited. Example: with a 2% spread and a 7% index gain, you’re credited 5% (subject to other limits).

- Fees: Most FIAs have no policy fee; income riders or enhanced rate features may charge an annual fee taken from your account value. Fees reduce return, so weigh the cost against the benefit.

Example: If the index gains 10% with a 50% participation rate and a 2% spread, your credited rate would be 3% (10% × 50% − 2%), subject to caps/floors.

If the index falls, your account value doesn’t go down for that period (assuming no excess withdrawals or charges).

Tip: Choose the index and crediting method that match your goals—greater growth potential vs. more consistent outcomes.

Why People Choose FIAs (Built for Retirees)

- Principal protection: No market‑loss during crediting periods.

- Steadier growth: Potential to outperform CDs over time—without stock‑market downside.

- Tax deferral: Pay taxes when you take withdrawals.

- Income options: Optional riders can provide guaranteed lifetime income you can’t outlive.

- Reminder: Review surrender periods, free‑withdrawal allowances, and any rider fees before purchasing.

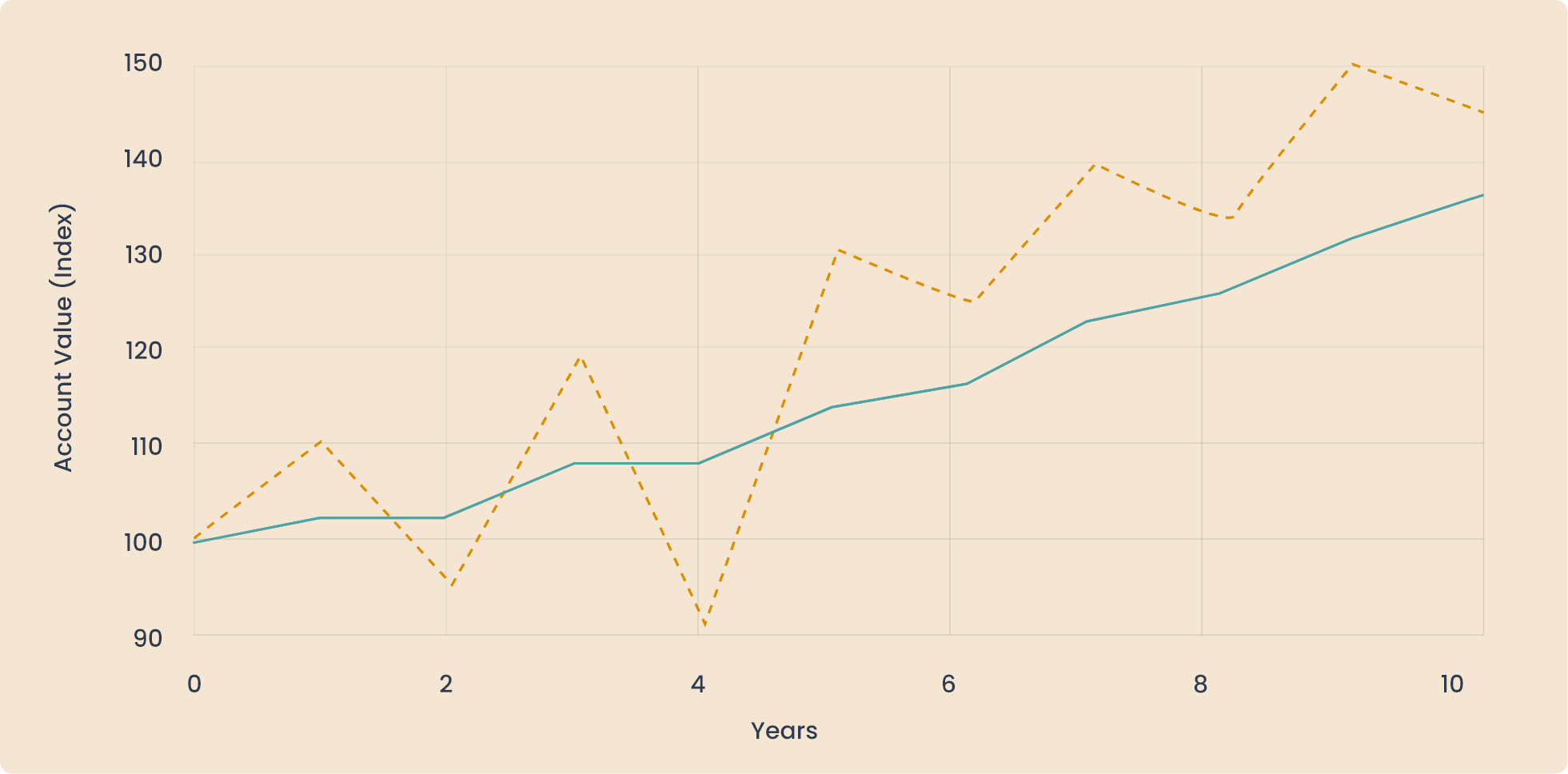

Live View

S&P 500 vs FIA with 8% Cap (Last 10 Years)

FIA credits assume a 0% floor and 8% annual cap for illustration. Actual products vary by issuer and contract.

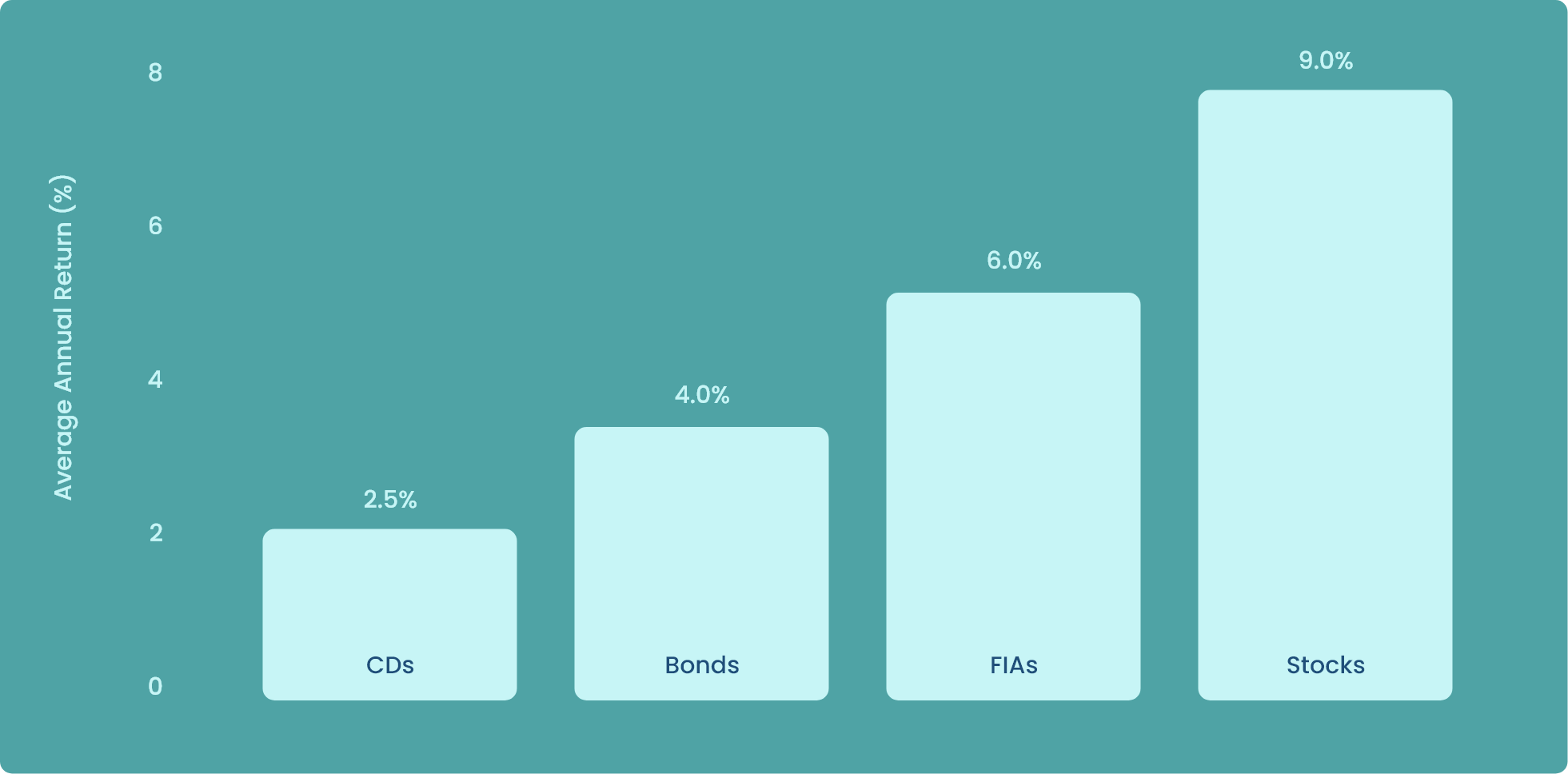

Historical Perspective

20‑Year Potential Returns: CDs, Bonds, FIAs, Stocks

CDs and Bonds shown via rate proxies; Stocks via index proxy; FIA modeled with 0% floor/8% annual cap. Results vary by period and product.

What Experts Say

Why it matters: Positions FIAs as a bond alternative when investors want principal protection with some growth potential.

Compare at a Glance

Where Each Option Fits

| Vehicle | Principal Protection | Growth Potential | Risk | Typical Use |

|---|---|---|---|---|

| Where Each Option Fits | Yes | Moderate | Low | Bond alternative for principal safety with some equity‑linked upside; optional lifetime income. |

| CDs | Yes | Low | Very Low | Short‑ to medium‑term guaranteed savings; early withdrawal penalties may apply. |

| Bonds | Depends† | Low–Moderate | Low–Moderate | Income and diversification; market value may fall when interest rates rise. |

| Variable Annuities | No* | Moderate–High | Moderate–High | Tax deferral; riders can add protections (*optional). |

| Stocks | No | High | High | Long‑term growth and wealth building; higher volatility. |

Education only; features vary by issuer and contract.

* Variable annuities: base contracts generally have no principal protection; optional riders (at additional cost) may add limited guarantees—terms, fees, and conditions apply.

† Bonds: “Depends” reflects issuer quality (e.g., government vs. corporate), maturity, and credit risk. Bond principal is not backed by government/insurer guarantees; market value can fluctuate.

We make it easier to compare and buy annuities in one place

We make it easier to compare and buy annuities in one place